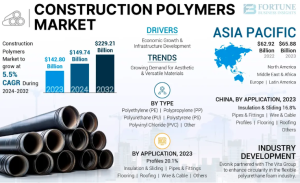

According to Fortune Business Insights, The global construction polymers market size was valued at USD 142.80 billion in 2023. The market is projected to grow from USD 149.74 billion in 2024 to USD 229.21 billion by 2032 at a CAGR of 5.5% during the forecast period. Asia Pacific dominated the construction polymers market with a market share of 46.13% in 2023.

Construction polymers, including elastomers, resins, and plastics, are vital in modern construction due to their durability and versatility. They withstand harsh conditions while promoting sustainability, such as improving energy efficiency in insulation. The market is expected to ramp up owing to rising adoption of such products in diverse applications, such as profiles and wire & cable.

Fortune Business Insights™ provides this information in its research report, titled “Construction Polymers Market, 2024-2032”.

Request a FREE Sample Copy: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/construction-polymers-market-110702

List of Key Players Mentioned in the Report:

- B. Fuller Company (U.S.)

- Solvay S.A. (Belgium)

- BASF SE (Germany)

- Evonik Industries AG (Germany)

- Reliance Industries Limited (India)

- SABIC (Saudi Arabia)

- Exxon Mobil Corporation (U.S.)

- Eni S.p.A (Italy)

- TotalEnergies (France)

- Avient Corporation (U.S.)

Segmentation:

Polyvinyl Chloride (PVC) Segment Dominated due to Technological Advancements

On the basis of type, the market is fragmented into Polyethylene (PE), Polypropylene (PP), Polyurethane (PU), Polystyrene (PS), Polyvinyl Chloride (PVC), and others. In 2023, the Polyvinyl Chloride (PVC) segment secured the key construction polymers market share as advances in polymer technology enhanced PVC’s functionality and environmental profile.

Pipes & Fittings Segment Dominated owing to Diverse Applications

In terms of application, the market is fragmented into profiles, pipes & fittings, insulation and sliding, flooring, roofing, wire & cable, and others. In 2023, the pipes & fitting segment captured the key construction polymers market share. The wide range of applications, including water supply, plumbing, and HVAC systems, supports continued demand for polymer-based pipes and fittings.

Polymers can be tailored to a variety of specifications, making them suitable for a vast array of construction applications, from insulation, sealants, and coatings to more structural components such as polymer concrete and composites.

In terms of region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Report Coverage:

The research report offers:

- Detailed examination of market trends and notable industry developments.

- Comprehensive coverage of factors contributing to recent market growth.

- Identification of emerging opportunities and challenges within the market.

- Evaluation of key market players, their strategies, and market positioning.

- Analysis of technological advancements shaping the market landscape.

Drivers and Restraints:

Economic Growth and Infrastructure Development to Impel Market Growth

The growing number of infrastructure developments, such as highways, bridges, and high-rise buildings, drives up demand for versatile and lightweight construction polymers. Moreover, economic growth boots the need for new residential, commercial, and public infrastructure, further increasing the demand for the product.

However, new government regulations aimed at environmental sustainability and safety may restrict the use of certain polymers, increasing costs and limiting construction polymers market growth.

Regional Insights:

Asia Pacific Dominated the Market Owing to Increasing Polymer Consumption in India

In 2023, Asia Pacific region led the construction polymers market and was valued at USD 65.88 billion in 2023. The region’s market growth is driven by China’s manufacturing dominance and India’s increased polymer consumption due to industrialization and rising incomes.

Latin America’s market growth is attributed to the rising demand for roofing and profiles in new construction projects, particularly in Mexico, Argentina, and Brazil, which are major market drivers.

Competitive Landscape:

Industry Participants Focus on Investments to Boost Product Performance

The competitive landscape shows a consolidated market where global players invest heavily in advanced technologies to enhance product performance. Key strategies include developing novel technologies and pursuing acquisitions and expansions to boost market share.

Information Source: https://www.fortunebusinessinsights.com/construction-polymers-market-110702

Key Industry Development:

- December 2023 – Reliance Industries Limited (RIL) became the first Indian company to chemically recycle plastic waste-based pyrolysis oil into International Sustainability & Carbon Certification (ISCC)-Plus certified Circular Polymers. This milestone demonstrates its commitment to reducing plastic waste and supporting the Circular Economy in India.

- September 2023 – ExxonMobil’s Baytown Texas facility started new chemical production units. The new performance polymers line would produce 400,000 metric tons per year of Vistamaxx and Exact branded polymer modifiers, enhancing the performance of various chemical products used in automotive parts, construction materials, and packaging applications.